Get Paid. Not Played.

We Work For You. Not the Insurance Company.

Get What You Deserve and Minimize Your Stress: Your Trusted Public Adjusting Firm

Don't Settle For Less With The Insurance Companies

Vandalism & Burglary

Get your Free Consultation

Compensation You Deserve

We ensure our clients receive the compensation they deserve. Here are some examples of claims we've expertly managed, showcasing our commitment to securing the best possible outcomes for our clients.

Insurance Companies we Work With

Maximum Settlement

Our team's expertise and dedication have consistently resulted in delivering the maximum possible settlement amount, ensuring our clients receive the compensation they truly deserve.

Licensed Service Areas

California

Nevada

Ohio

Fire/Smoke Damage

Water Damage

Wind/Roof Damage

Vandalism/Burglary

Thank you. We will reach out shortly.

Blog

Expert claim guidance, property damage insights, and insurance tips to help policyholders protect their recovery.

What is a Public Adjuster?

May 25, 2026

Does Insurance Cover Wildfire Smoke Damage in Los Angeles if the Home Did Not Burn?

June 15, 2026

Maximum Settlement

Our team's expertise and dedication have consistently resulted in delivering the maximum possible settlement amount, ensuring our clients receive the compensation they truly deserve.

Claim Types

We specialize in a plethora of claim types.

Fire/Smoke/Ash Damage

Water Damage

Wind Damage

Vandalism/Burglary

Personal Property

Maximum Settlement

Our team's expertise and dedication have consistently resulted in delivering the maximum possible settlement amount, ensuring our clients receive the compensation they truly deserve.

Locations

We are licensed in the state of California but mainly service the locations below.

Beverly Hills

Burbank

Calabasas

Glendale

Granada Hills

Hollywood

Los Angeles

Pasadena

Palm Springs

Maximum Settlement

Our team's expertise and dedication have consistently resulted in delivering the maximum possible settlement amount, ensuring our clients receive the compensation they truly deserve.

Case Studies

Real claims. Real obstacles. Documented recoveries where policyholders were initially underpaid, delayed, or denied.

Failed Dishwasher Supply Line

(Water Damage)

Settled $311,307.12

Altadena Fire 2026

(Smoke Damage)

Settled $71,456.96

Ceiling Pipe Burst

(Water Damage)

Settled $115,406.37

Palisades Fire 2026

(Smoke Damage)

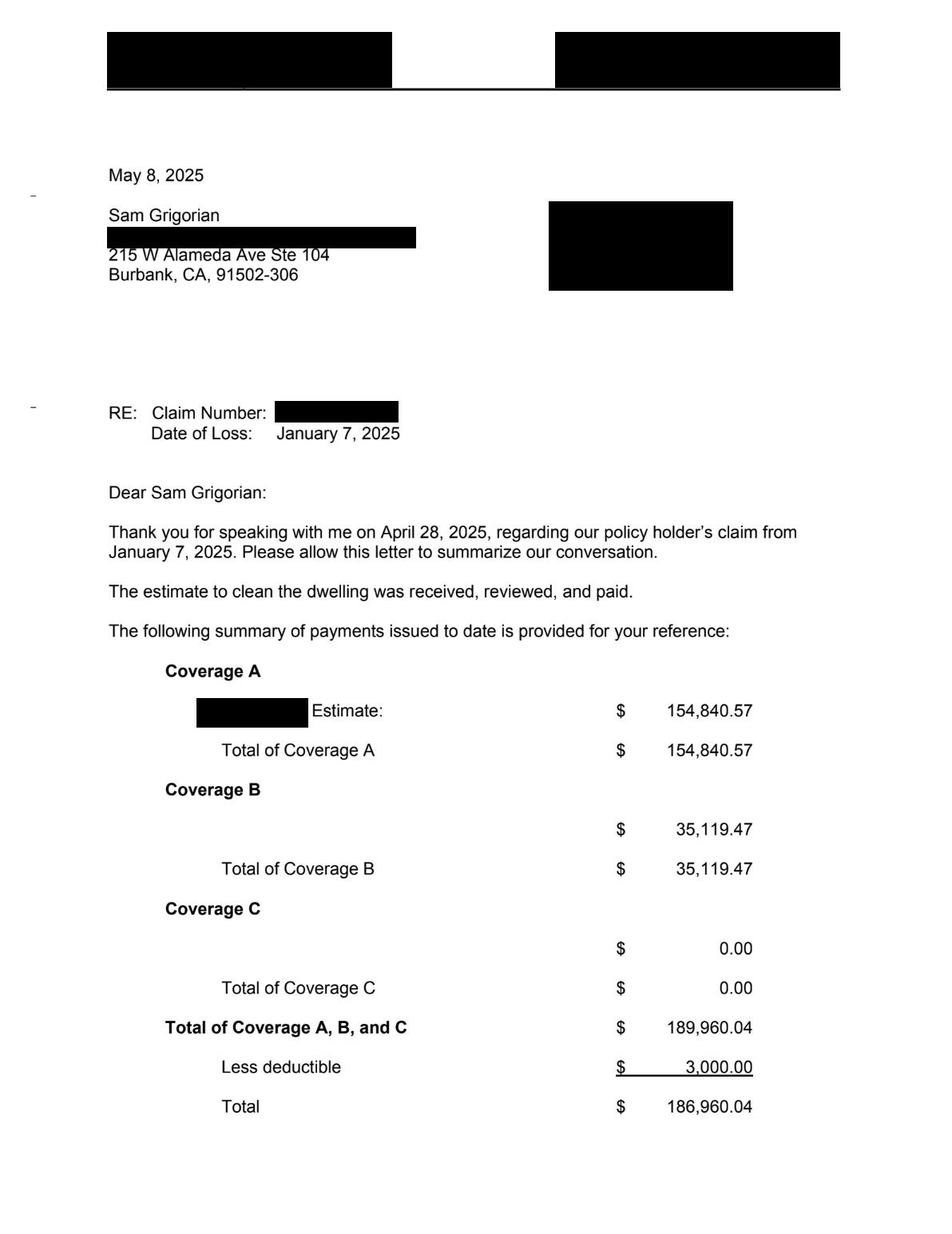

Settled $186,960.04

Altadena Fire 2026

(Smoke Damage)

Settled: $93,244.73

Maximum Settlement

Our team's expertise and dedication have consistently resulted in delivering the maximum possible settlement amount, ensuring our clients receive the compensation they truly deserve.

Does Insurance Cover Wildfire Smoke Damage in Los Angeles if Your Home Did Not Burn?

June 15, 2026

Yes, a Los Angeles homeowner may have a wildfire smoke damage insurance claim even if the home did not burn. Coverage depends on the policy, the facts of the loss, and the damage documentation. Smoke, soot, ash, odor, HVAC contamination, attic residue, contents damage, pool contamination, and exterior staining can all become part of a disputed wildfire smoke claim.After the Eaton Fire and Palisades Fire, many Los Angeles property owners were left dealing with smoke and ash exposure even when their homes were outside the burn area. These claims can be difficult because the damage is not always obvious during a quick inspection. Smoke particles, soot residue, and odor can affect interior surfaces, furniture, clothing, electronics, ductwork, attic spaces, roofing, exterior finishes, and personal property.A proper smoke damage claim should be documented before the property is cleaned or repaired. Homeowners should take photos and videos, save damaged HVAC filters, list affected contents, document smoke odor by room, photograph ash or soot residue, keep food spoilage records, and save all cleaning, inspection, and repair estimates. If the insurance company’s estimate does not include contents cleaning, HVAC review, attic inspection, roof cleaning, exterior cleaning, pool cleaning, or odor treatment, the claim may need further review.One common issue in Los Angeles wildfire smoke damage claims is that the carrier’s first estimate may not include the full scope of work. The insurance company may allow limited cleaning while excluding hidden contamination, disputed contents, odor treatment, exterior surfaces, or specialty cleaning. Before accepting a settlement, homeowners should understand what was inspected, what was excluded, and whether the estimate actually accounts for restoring the property to its pre-loss condition.Ares helps Los Angeles property owners with wildfire smoke damage insurance claims, including smoke, soot, ash, odor, contents damage, roof and exterior issues, pool contamination, and underpaid or delayed carrier estimates. If your home was affected by wildfire smoke or ash, request a free claim review before settling your claim.

Frequently Asked Questions About Wildfire Smoke Damage Claims

Does homeowners insurance cover smoke damage from a nearby wildfire?

It may, depending on the policy, cause of loss, and documented damage. A home does not always need direct flame damage for smoke, soot, ash, or odor issues to be part of an insurance claim.

What should I document for a wildfire smoke damage claim?

Document visible soot, ash, smoke residue, odor, damaged contents, HVAC filters, attic areas, exterior surfaces, pool contamination, food spoilage, cleaning estimates, and all communications with the insurance company.

Should I clean smoke damage before the insurance adjuster inspects?

Avoid major cleaning before the damage is documented. Take photos and videos first, save receipts, and keep samples or records of affected filters, contents, and cleaning needs.

What if the insurance company’s estimate seems too low?

If the estimate excludes contents cleaning, odor treatment, HVAC review, attic inspection, exterior cleaning, pool cleaning, or other affected areas, the claim may be under-scoped. A public adjuster can review the estimate and help document the full loss.

When should I call a public adjuster for a smoke damage claim in Los Angeles?

Consider calling a public adjuster if the carrier denies part of the claim, delays the claim, issues a low estimate, disputes smoke or soot contamination, excludes contents, or fails to inspect all affected areas.

What Is a Public Adjuster? What Do Public Adjusters Do?

May 25, 2026

When property damage happens, the insurance claim process can feel confusing, slow, and one-sided. A public adjuster is a licensed insurance claims professional who represents the policyholder, not the insurance company.At Ares Public Adjusters, we help homeowners and business owners in Los Angeles document property damage, prepare insurance claims, communicate with the insurance company, and pursue a fair settlement under the policy.

What Does a Public Adjuster Do?

A public adjuster helps manage the insurance claim from the policyholder’s side. This may include:Reviewing the insurance policy to understand coverage, exclusions, limits, and claim requirements.Inspecting and documenting damage to the property.Preparing estimates, inventories, photographs, reports, and other claim support.Communicating with the insurance company and its adjusters.Negotiating the claim settlement on behalf of the policyholder.Helping dispute underpaid, delayed, or denied claims when the facts and policy support further recovery.The goal of a public adjuster is to help the insured present a complete and properly documented claim.

Public Adjuster vs. Insurance Company Adjuster

The main difference is who the adjuster represents.An insurance company adjuster works for the insurance company or is assigned by the insurance company. A public adjuster is hired by the policyholder and represents the policyholder’s interests in the claim.This distinction matters because property insurance claims often involve detailed estimating, policy interpretation, documentation deadlines, and negotiation. A public adjuster helps the insured avoid relying only on the insurance company’s evaluation of the damage.

When Should You Hire a Public Adjuster?

You may want to contact a public adjuster if:Your home or business suffered fire, water, smoke, storm, theft, vandalism, or other property damage.The insurance company’s estimate seems too low.The claim is delayed, disputed, or denied.You are unsure what your policy covers.You do not have time to manage the claim yourself.The damage is significant and requires detailed documentation.For Los Angeles property owners, claims can be especially complex because homes and commercial buildings often involve high repair costs, code issues, specialty materials, business interruption concerns, and multiple types of damage.

What Types of Claims Can Ares Public Adjusters Help With?

Ares Public Adjusters assists with many types of property insurance claims in Los Angeles, including:Fire and smoke damage claims.Water damage claims.Roof and storm damage claims.Theft and burglary claims.Vandalism claims.Commercial property claims.Residential property claims.Denied or underpaid insurance claims.Each claim is different. The best first step is to have the damage, policy, and insurance company position reviewed before accepting a final settlement.

Why Work With Ares Public Adjusters?

Ares Public Adjusters is a Los Angeles public adjusting firm focused on helping policyholders through the property insurance claim process. We work to make the claim clear, organized, and properly supported with documentation.If you are dealing with property damage, you do not have to handle the insurance claim alone. A public adjuster can help you understand the process, protect your rights under the policy, and present your claim with the detail it deserves.

Why Work With Ares Public Adjusters?

If you need help with a property damage claim in Los Angeles, contact Ares Public Adjusters for a claim review.Ares Public Adjusters represents policyholders, not insurance companies.

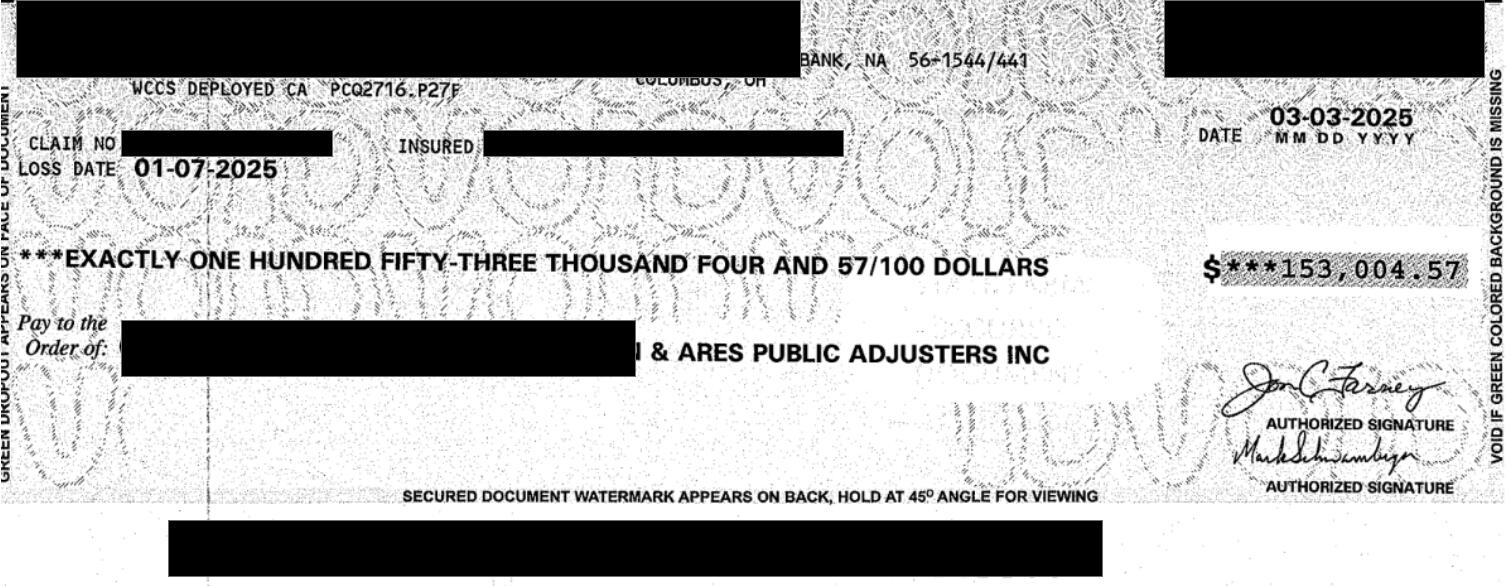

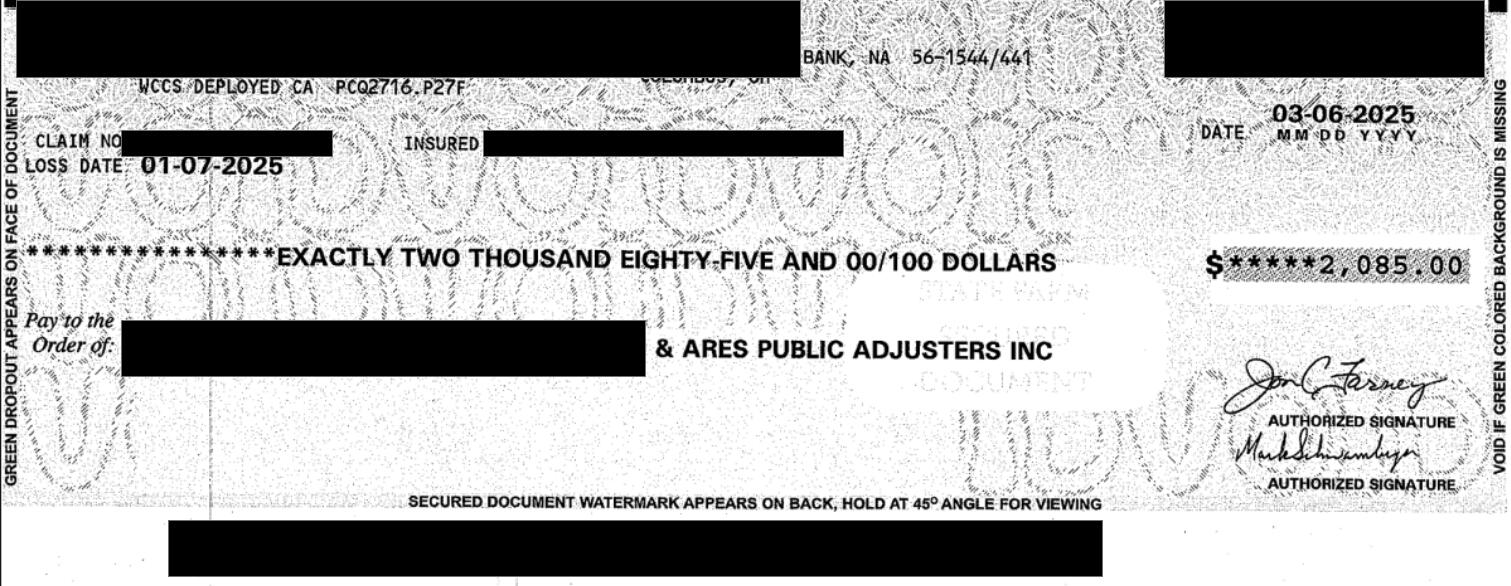

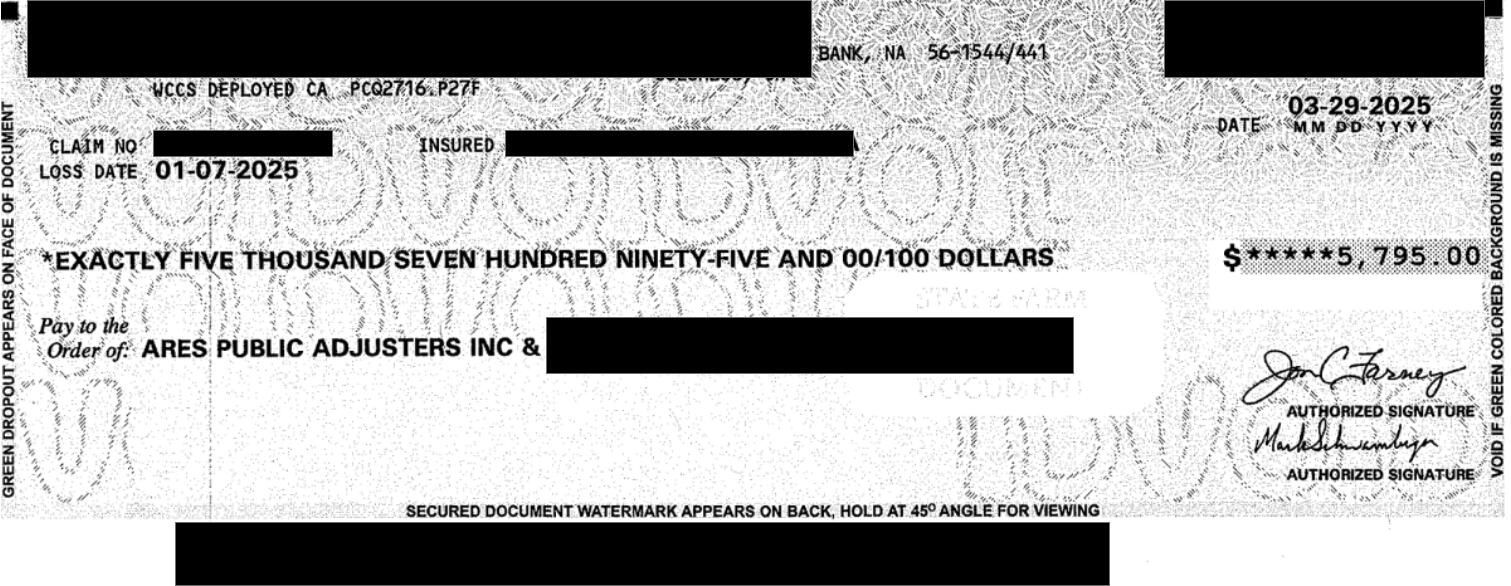

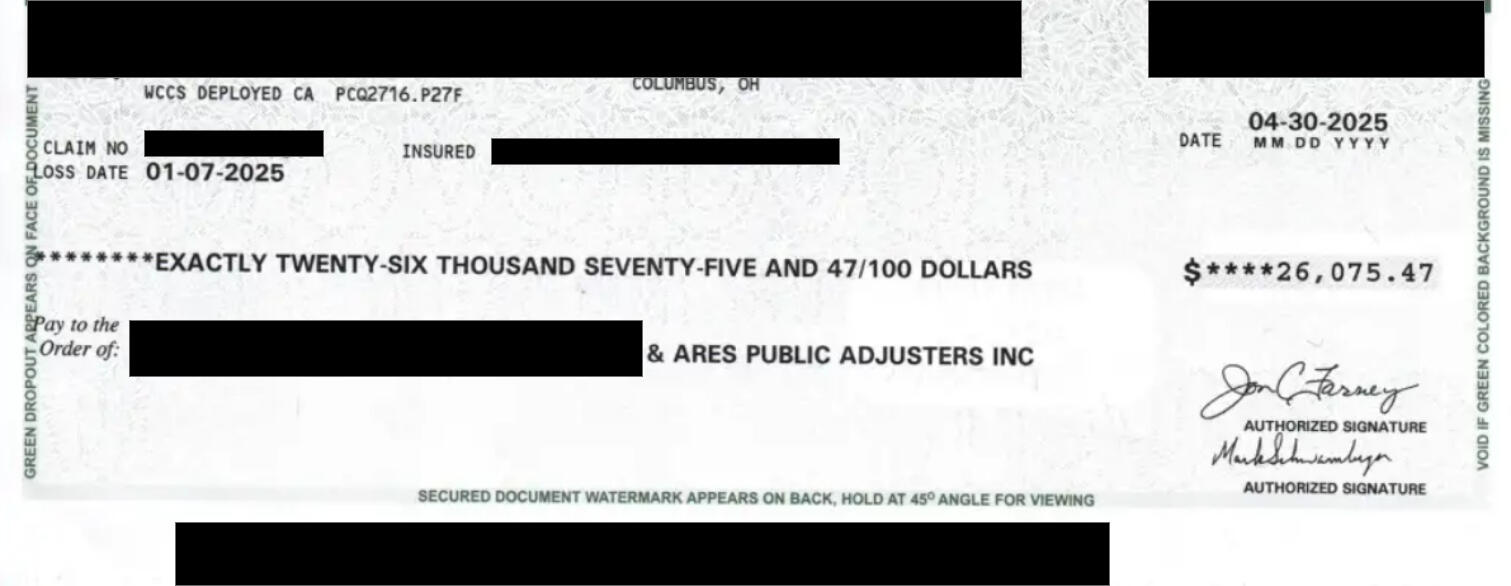

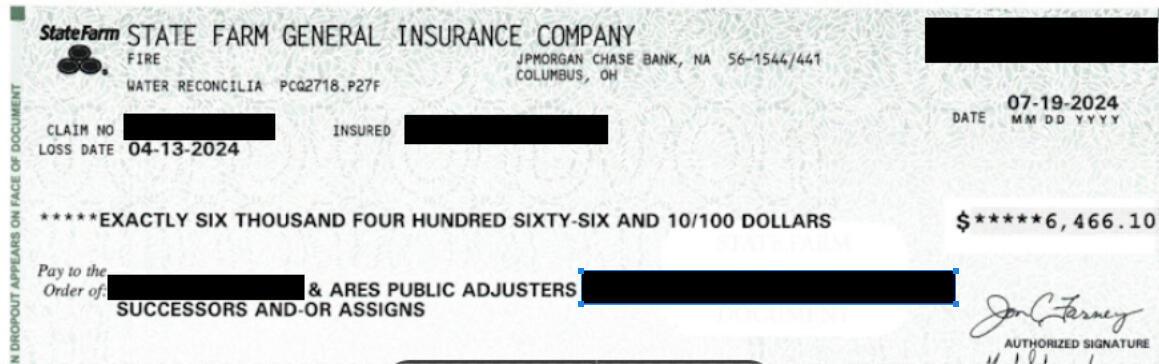

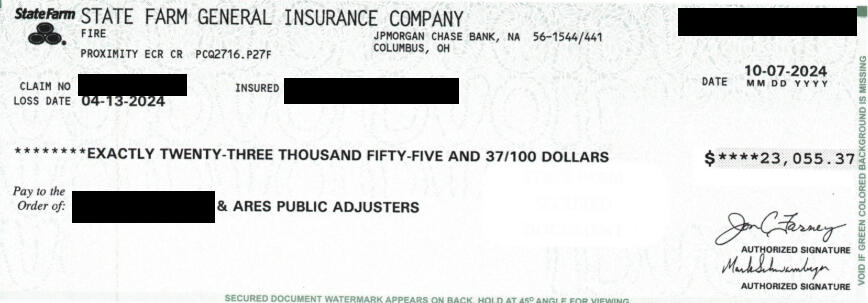

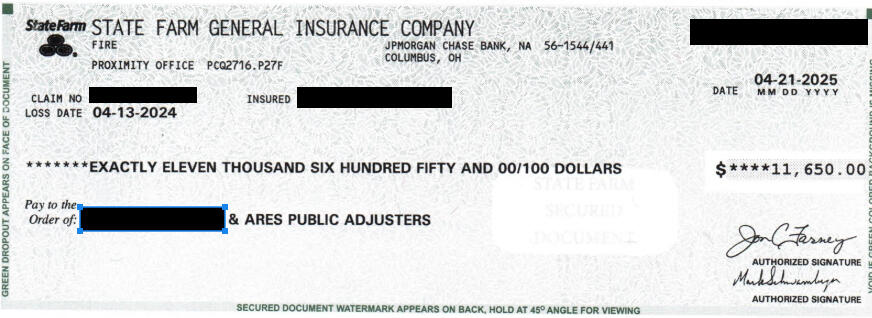

Settled $93,244.73

Smoke Damage Settlement for a Los Angeles Area Home After the Eaton Fire

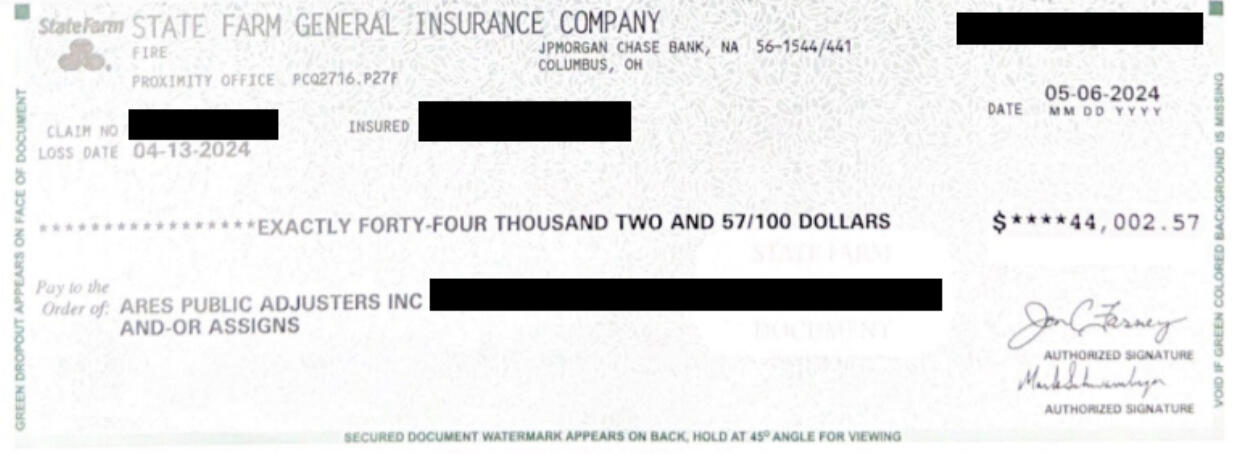

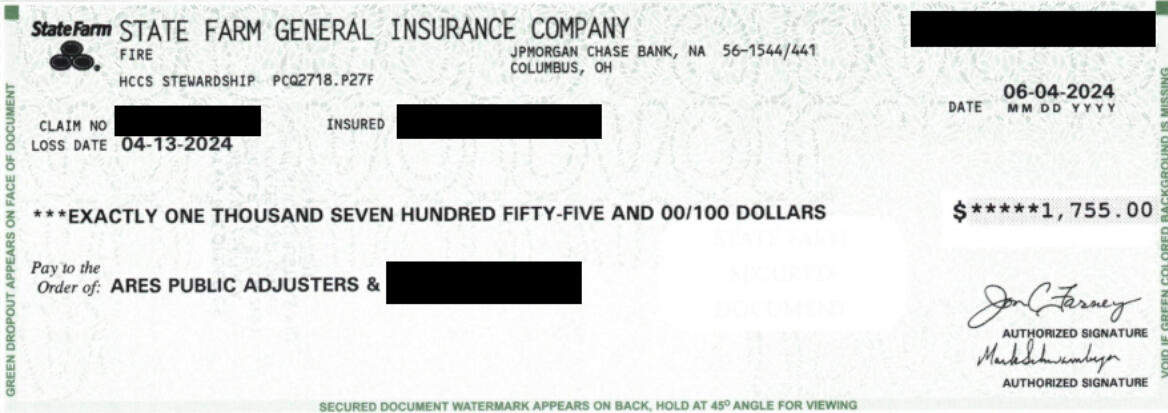

Wildfire smoke damage is not always limited to homes directly burned by flames. In this claim, a 2,102 sq. ft. home located approximately five miles from the Eaton Fire sustained heavy smoke and soot contamination. Although the structure was not consumed by fire, the property required extensive cleaning, contents restoration, pool cleaning, and additional claim support for food spoilage caused by an electricity outage.The date of loss was January 7, 2025. The carrier initially pushed back on portions of the cleaning scope, including the level of cleaning required, exterior and roof cleaning, attic-related items, and certain equipment-related charges. After continued documentation, estimate review, follow-up, and supplement work, the total settlement reached $93,244.73.

Gutter Ash Contamination

Exterior Chemical Sponge Test

The Problem: Smoke and Soot Contamination Even Miles From the Fire

This Los Angeles-area home was located roughly five miles from the Eaton Fire, but the distance did not prevent smoke and soot from affecting the property. Wildfire smoke can travel, settle, and contaminate building surfaces, personal property, HVAC-related areas, exterior components, pool systems, and household contents.The insured had cleaning work involved early in the process, and a restoration estimate, inspection photos, food-loss information, and additional supporting documentation were submitted to the claim file. Even with that documentation, the carrier did not simply approve every requested item without dispute.

Window Seal Chemical Sponge Test

Client's Mirror Swab

Carrier Pushback on the Smoke Damage Scope

The carrier challenged several parts of the smoke and soot cleaning estimate. The disputed items included:Changing heavy cleaning to normal cleaning.Reducing or changing exterior and roof cleaning scope.Objecting to pressure washing because of possible damage to the exterior or roof.Removing certain attic sealing or stain-blocking items.Removing hydroxyl generator-related items.Requesting additional documentation for food spoilage caused by the electricity outage.This type of pushback is common in Los Angeles smoke damage claims, especially when a property is not directly burned by the wildfire. The dispute often shifts from whether a fire occurred to how much smoke and soot remediation is actually required.

Our Approach

The claim required persistent follow-up and a practical response to the carrier’s objections. The strategy focused on documenting the actual cleaning needs and resolving scope disagreements without losing legitimate covered damage.Key steps included:Submitting the restoration estimate and inspection photo report.Following up repeatedly while the estimate remained under review.Submitting the pool cleaning estimate as a separate scope item.Pursuing the contents cleaning estimate until payment was issued.Addressing the carrier’s objections to heavy cleaning.Revising the roof and exterior cleaning approach where pressure washing was challenged.Supporting the food spoilage portion of the claim after the outage.Continuing supplement negotiations until additional dwelling cleaning money was issued.One important issue involved the roof and exterior cleaning. The carrier objected to pressure washing because it could damage the roof or exterior. Instead of abandoning the item, the scope was revised to account for manual cleaning. That preserved the substance of the claim while addressing the carrier’s stated concern.

The Result: $93,244.73 Total Settlement

The claim ultimately resolved for $93,244.73 across dwelling cleaning, pool cleaning, contents cleaning, a dwelling cleaning supplement, and food spoilage.The largest portion of the settlement was for dwelling cleaning, followed by contents cleaning and a dwelling cleaning supplement. The final result also included payment for pool cleaning and food spoilage tied to the electricity outage.This was a relatively straightforward smoke damage claim based on the level of contamination, but it still required follow-up, documentation, and pushback against scope reductions.

Heavily Contaminated Air Filter

Why This Case Matters for Los Angeles Smoke Damage Claims

A home does not need to burn down to suffer a serious smoke damage loss. Smoke and soot can create cleaning, deodorization, contents, HVAC, pool, and exterior remediation issues even when the property is several miles away from the wildfire perimeter.For homeowners dealing with smoke damage in Los Angeles, the most important issue is not only proving that smoke reached the property. It is proving the full scope of cleaning and restoration required under the policy.That usually means documenting:Interior smoke and soot contamination.Exterior residue and roof-related cleaning needs.Contents affected by smoke or odor.Pool contamination from ash, soot, or debris.HVAC or air circulation concerns.Food spoilage from a related power outage.Cleaning estimates from qualified vendors.Photos, reports, receipts, and claim communications.

Common Mistake Homeowners Make After Wildfire Smoke Damage

Many homeowners assume that if the carrier accepts part of the smoke claim, the rest of the scope will be handled automatically. This case shows why that assumption can be costly.The carrier may pay an initial dwelling cleaning amount but still dispute contents, pool cleaning, roof cleaning, heavy cleaning, equipment charges, or supplements. A partial payment does not always mean the full claim has been properly valued.

Frequently Asked Questions About Los Angeles Smoke Damage Claims

Can a home have a valid smoke damage claim if it was miles away from the fire?

Yes. A property can still suffer smoke and soot contamination even if flames never reached the structure. The key issue is whether the smoke, soot, ash, or related contamination caused covered damage under the policy and whether the scope is properly documented.

What should be included in a wildfire smoke damage claim?

Depending on the facts, a smoke damage claim may include dwelling cleaning, contents cleaning, HVAC evaluation, exterior cleaning, pool cleaning, odor treatment, and food spoilage from an electricity outage. The exact scope depends on the damage, the policy, and the supporting documentation.

Why do insurance companies reduce smoke damage estimates?

Carriers may reduce estimates by changing heavy cleaning to standard cleaning, removing odor treatment equipment, rejecting certain exterior cleaning methods, disputing contents cleaning, or requesting additional proof. These reductions can often be challenged with photos, vendor estimates, reports, and detailed claim documentation.

Final Settlement Summary

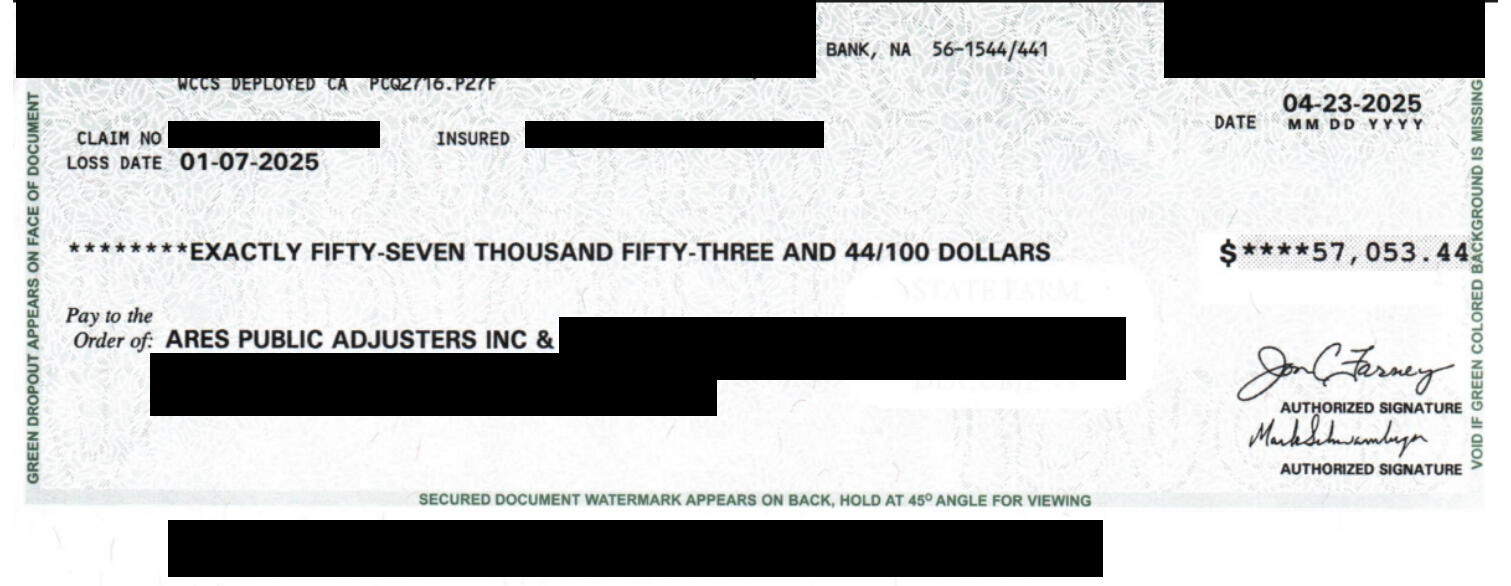

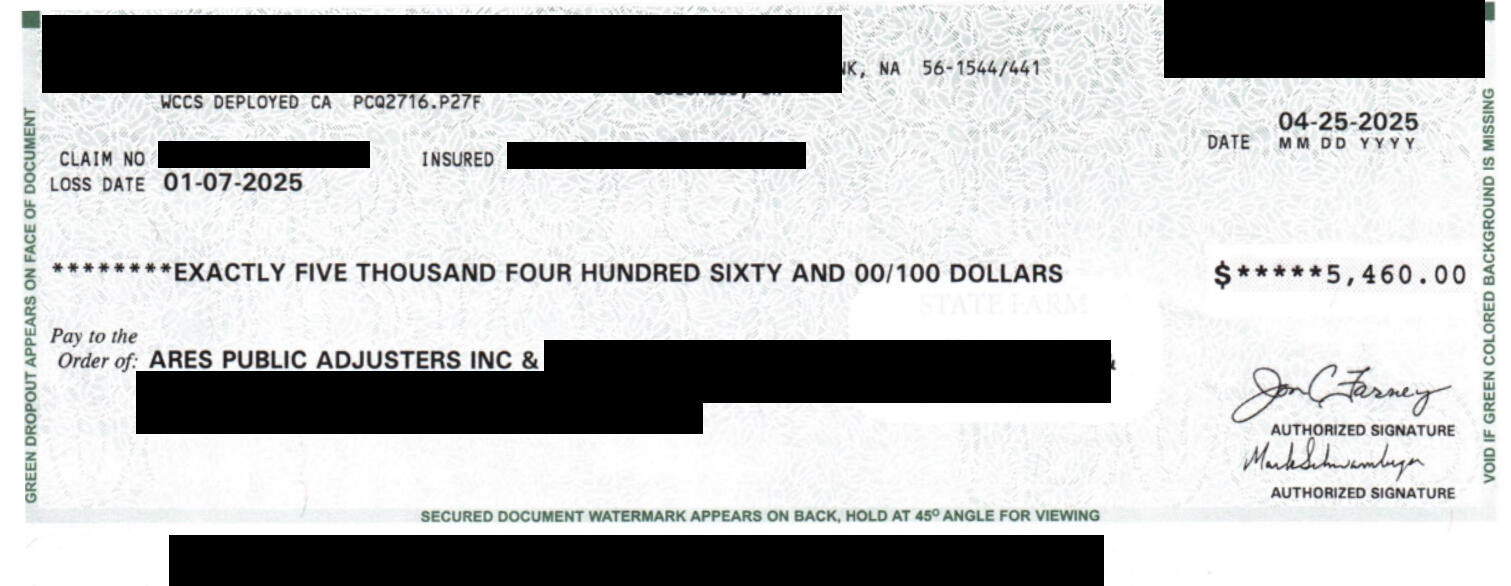

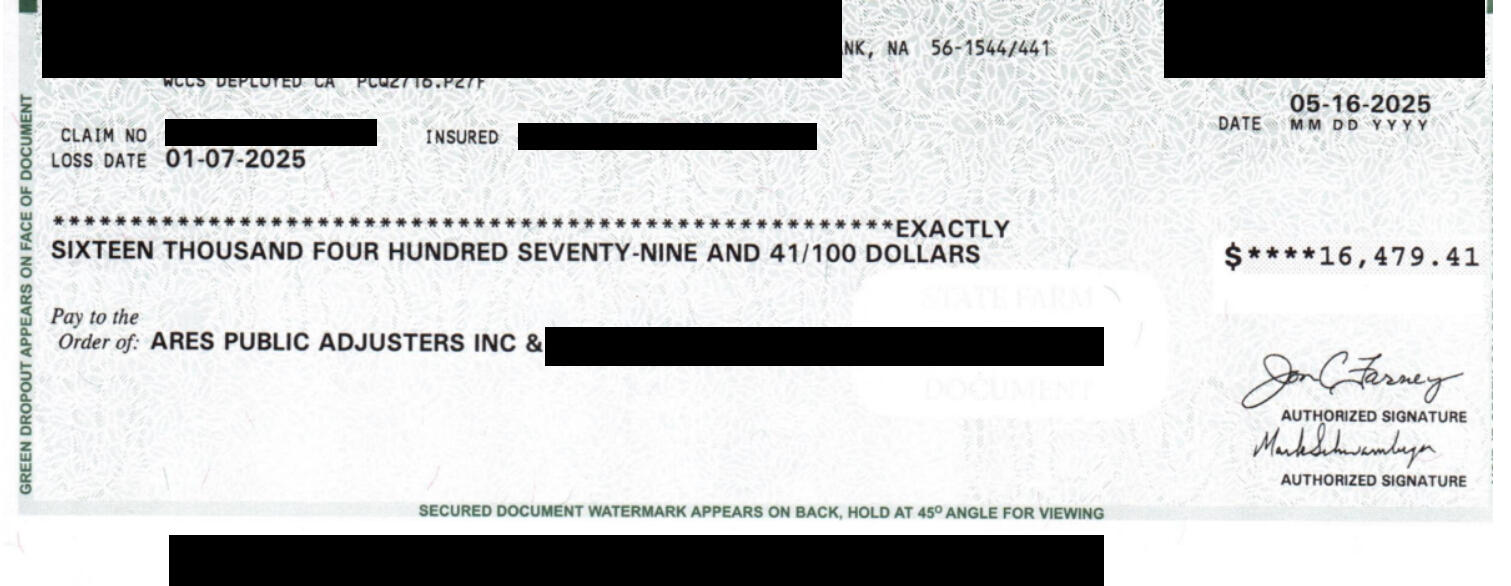

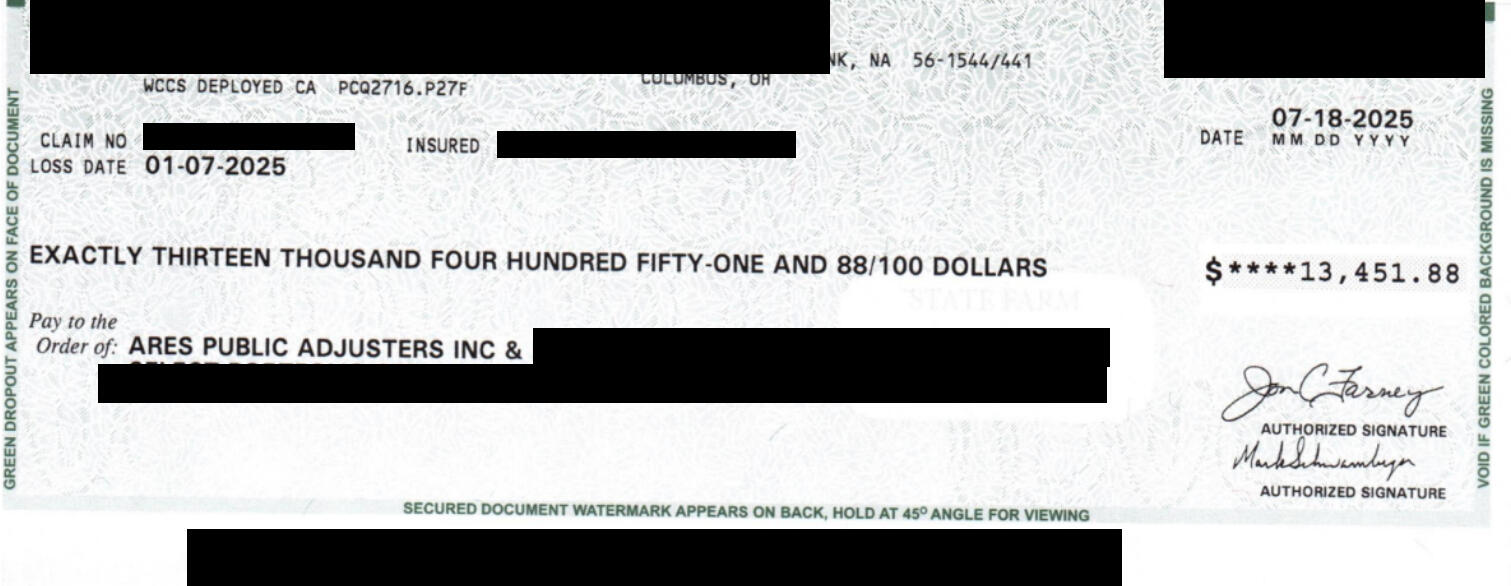

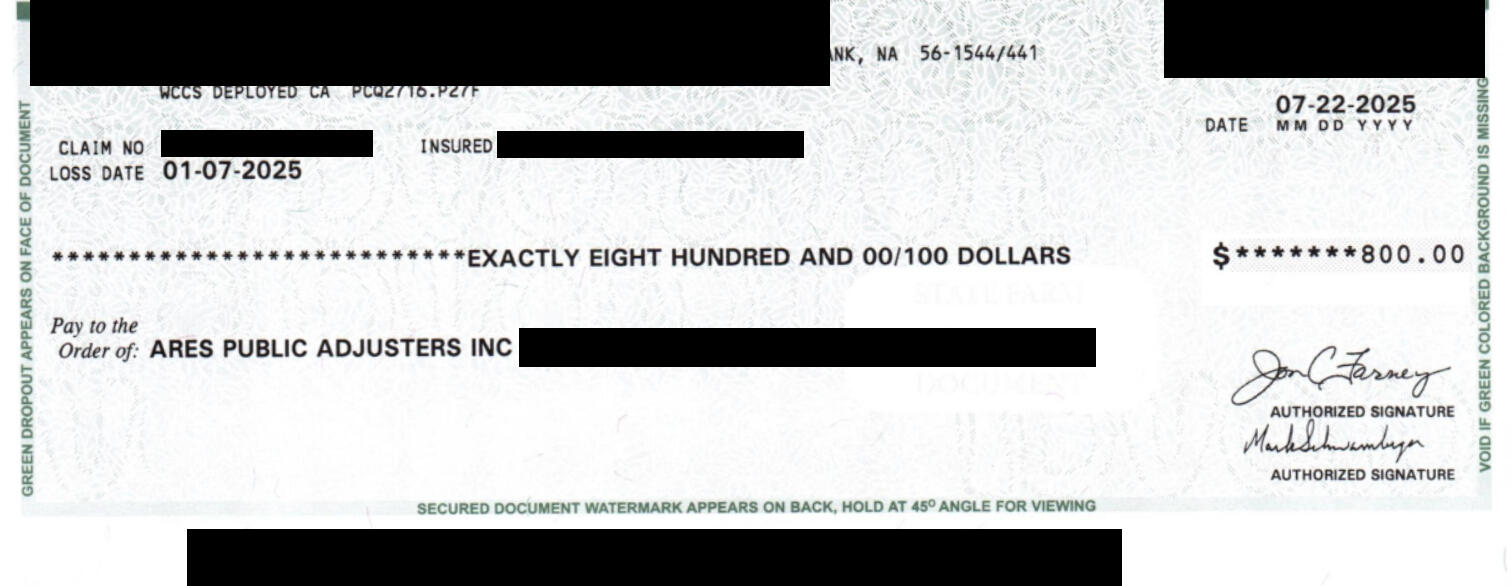

This Eaton Fire smoke damage claim involved a 2,102 sq. ft. Los Angeles-area home located approximately five miles from the fire. Despite carrier pushback on the scope of cleaning and related items, the claim resolved for a total settlement of $93,244.73.The outcome included:$57,053.44 for dwelling cleaning.$5,460.00 for pool cleaning.$16,479.41 for contents cleaning.$13,451.88 for a dwelling cleaning supplement.$800.00 for food spoilage from the electricity outage.Every smoke damage claim is different, and no result is guaranteed. But this case shows why documentation, estimate review, and persistent supplement work matter when a Los Angeles homeowner is dealing with wildfire smoke and soot contamination.

Initial Dwelling Cleaning Check

Pool Cleaning Check

Contents Cleaning Check

Dwelling Cleaning Supplement Check

Food Spoilage Check

Settled $186,960.04

Palisades Fire Smoke, HVAC, Pool, and Interior Damage

Date of Loss: January 7, 2025

Cause of Loss: Smoke damage from the Palisades Fire

Property Size: 2,769 square feetOn January 7, 2025, a homeowner near the Palisades Fire suffered smoke damage to a 2,769 square foot residential property. The home was close enough to the fire activity that smoke, ash, and residue affected several parts of the property, including the exterior, interior, HVAC system, and pool.This was not a simple wipe-down claim. The damage was spread throughout the property, and several important items needed to be documented properly before the insurance carrier could fully evaluate the loss.

Ash & Char in Client's Pool

Ash & Char in Client's Attic

What Happened

After the Palisades Fire, the homeowner noticed smoke residue and contamination throughout the property. The exterior had visible smoke and ash exposure, and the interior also showed signs of smoke impact.One of the biggest concerns was the HVAC system. Because the system moves air throughout the home, smoke and ash exposure can create continuing odor and contamination issues if it is not inspected and addressed correctly. In this case, the HVAC system was severely impacted and needed to be treated as a major part of the claim, not a minor cleaning issue.The pool was also affected by the wildfire conditions. Ash, smoke residue, and debris entered the pool area, requiring professional cleaning instead of routine maintenance.Areas of DamageThe claim involved several categories of smoke-related damage:Interior smoke residue and odor concernsExterior smoke and ash contaminationHVAC system contaminationPool contamination from smoke, ash, and debrisPotential attic and insulation exposureContents and textile-related smoke impactAdditional cleaning and inspection items that needed follow-up

Outdoor Patio Ashe Damage

Close up of Ash

Why This Claim Required More Than a Basic Insurance Estimate

Smoke damage claims are often underestimated because much of the damage is not as obvious as fire damage. A home does not need to burn for the loss to be serious.In this case, the smoke had affected multiple systems and surfaces. The property needed a full smoke damage evaluation, including the HVAC system, pool, contents, and areas where smoke residue may have settled.The insurance claim had to be presented with enough detail to show that the damage was not limited to surface cleaning.

Our Role

Ares helped the homeowner document the full scope of the Palisades Fire smoke damage claim.Our work included reviewing the property damage, communicating with the insurance company, coordinating inspections, following up on missing items, and making sure the HVAC and pool issues were addressed as part of the claim.The HVAC system required particular attention because smoke contamination in an air system can continue affecting the home after other surfaces are cleaned. The pool also required follow-up because wildfire ash and smoke debris created a need for professional cleaning.

The Result

The claim was resolved after the smoke damage, HVAC impact, pool cleaning, and related claim items were documented and reviewed.For this homeowner, the important issue was making sure the insurance company looked at the entire property, not just the obvious surface-level smoke residue.

What Homeowners Should Know After the Palisades Fire

If your home was near the Palisades Fire, smoke damage may affect more than what you can see.Smoke and ash can enter the HVAC system, settle inside the attic, affect exterior finishes, contaminate pool water, and leave odor or residue inside the home. These items should be documented before repairs or cleaning are completed.A proper smoke damage claim should include a review of the full property, including mechanical systems, interior surfaces, exterior surfaces, contents, and outdoor areas such as pools and patios.

Need Help With a Palisades Fire Smoke Damage Claim?

Ares helps homeowners with wildfire smoke damage insurance claims in Pacific Palisades, Malibu, Santa Monica, Brentwood, Topanga, Los Angeles, and surrounding areas.If your property was affected by the Palisades Fire, your insurance claim may involve more than general cleaning. Smoke damage can impact the HVAC system, interior, exterior, pool, attic, and personal property.Contact Ares for help documenting and presenting your wildfire smoke damage insurance claim.

Insurance Settlement Letter

Initial Dwelling Cleaning Check

HVAC Cleaning Supplement Check

Pool Cleaning Check

Contents Cleaning Check

Settled $115,406.37

A Sudden Water Loss

On June 3, 2024, a pipe burst in the ceiling of a residential unit, causing extensive water damage throughout the interior. Water spread quickly through the ceiling cavity and into the living space, affecting multiple building components and requiring both emergency mitigation and a full rebuild of damaged areas.Emergency mitigation was performed immediately to dry the structure and prevent further deterioration. The mitigation contractor was ultimately paid $16,000 for the emergency services.

Ceiling Pipe in Living Room

Thermal Imaging

The Initial Estimate Gap

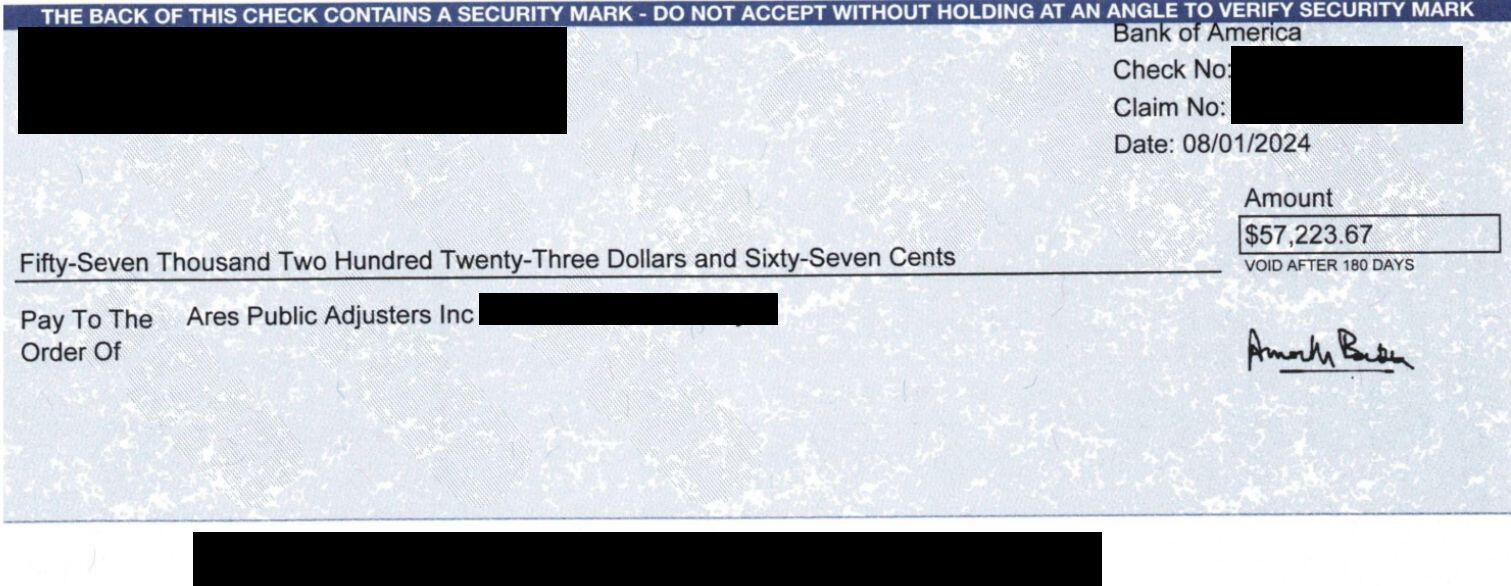

After inspecting the property, our team prepared a detailed rebuild estimate totaling:$104,723.78Despite the documented scope of damage, the insurance carrier initially issued a payment of:$57,223.67This amount represented only a partial valuation of the necessary repairs and left a substantial gap between the documented damage and the insurer's payment.

Moisture Meter of Ceiling

Air Movers & Dehumidifiers Mitigation

The “Unbiased” Comparative Bid

To justify their position, the carrier hired a vendor to produce a comparative estimate, which is commonly presented as an independent evaluation of the damage.However, during our review of the file we discovered a critical issue.The third party company coordinating the vendor had modified and removed essential repair line items from the vendor's estimate before it was finalized. These removed items included necessary repair components that were clearly supported by the damage documentation.This manipulation significantly reduced the apparent scope of work.

Challenging the Carrier's Findings

We disputed the altered estimate and raised the issue directly with the desk adjuster. After continued discussions and documentation of the missing scope items, the carrier agreed to bring in another vendor to perform a new evaluation of the rebuild costs.This second inspection produced a much more competent and comprehensive estimate.

Post Demolition Containment Barriers

A Second Vendor Confirms the Scope

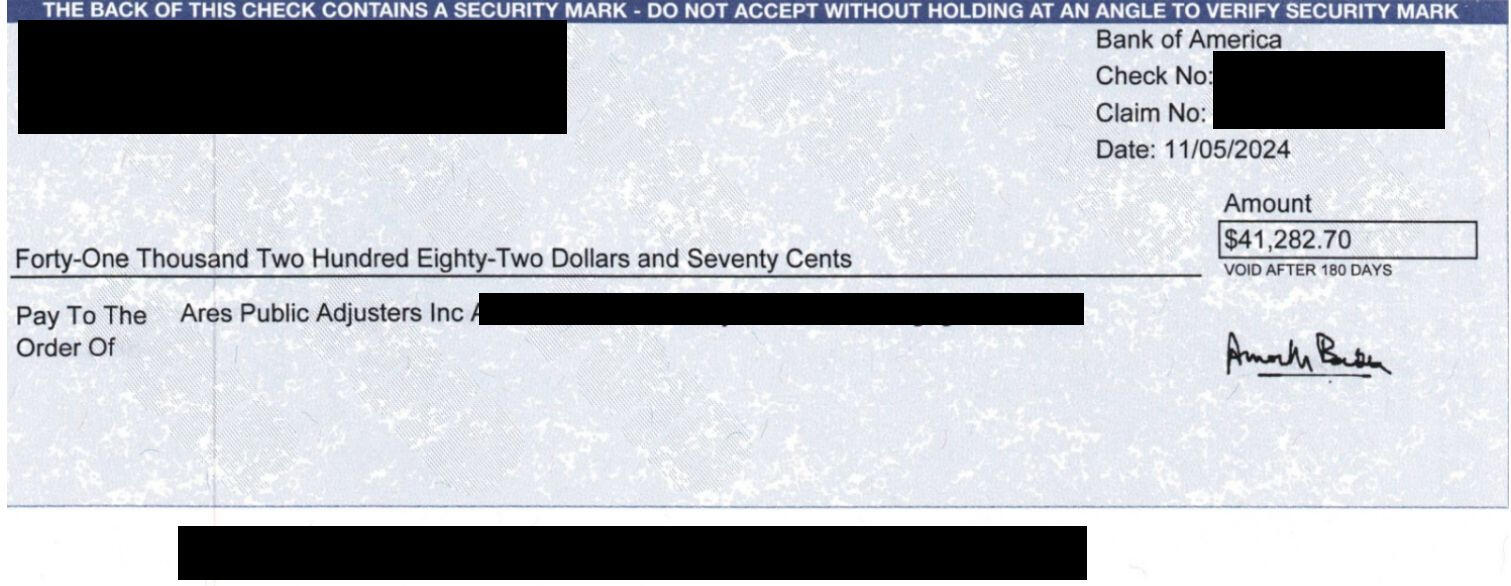

The second vendor's estimate came in very close to our documented rebuild amount, confirming that the original comparative estimate had undervalued the damage.Following this review, the carrier issued a supplemental payment of:$41,282.70

The Final Outcome

The carrier's total payments for the rebuild ultimately reached:Initial Payment

$57,223.67Supplemental Payment

$41,282.70Total Paid: $98,506.37Compared to our estimate of $104,723.78, the final carrier payment represented approximately:94% of our documented rebuild estimate

Initial Rebuild Check

Emergency Mitigation Services Check

Rebuild Supplement Check

Settled $71,456.96

Background

Following the Eaton Fire on January 7, 2025, the insured's property in Pasadena sustained heavy smoke contamination affecting both the structure and the contents inside the home. Smoke particulates spread throughout the interior, requiring professional cleaning, restoration evaluation, and documentation of both structural and personal property damage.In addition to the interior contamination, the property also sustained wind-related damage to the roof during the fire event. The roof and exterior components were heavily contaminated with wildfire smoke and soot. The home’s solar panel system was also significantly affected, requiring specialized cleaning to remove smoke residue and restore proper performance.Our team was retained by the homeowner to assist with the claim process and ensure that all smoke-related damage was properly documented and addressed with the insurance carrier.

Insured's Roof

Siding Soot Contamination

Initial Claim Handling

After engagement, the claim was opened with the carrier and inspections were coordinated. A photo report and restoration estimate prepared by a restoration contractor were submitted to the adjuster to document the extent of smoke contamination and cleaning requirements for the interior, roof surfaces, and solar panels.The carrier issued an initial payment related to the dwelling portion of the claim. However, the estimate prepared by the restoration contractor differed significantly from the carrier’s estimate.

Contaminated Solar Panels

Coverage Dispute

During the review process, a discrepancy of approximately $40,000 emerged between the carrier’s estimate and the restoration contractor’s estimate for smoke remediation work.The insurance company indicated that a third-party vendor would review the scope to address the discrepancy. Despite ongoing communication and documentation, the gap between the estimates remained unresolved.To move the claim forward, the matter proceeded to the appraisal process, a formal dispute resolution method outlined in most property insurance policies.

Interior Ash Contamination

Chemical Sponge Test

Appraisal Outcome

Through appraisal, the disputed scope and costs were evaluated independently. The process resulted in additional funds being awarded for the dwelling smoke cleaning work, helping bridge the gap between the original carrier estimate and the documented remediation needs.

Claim Result

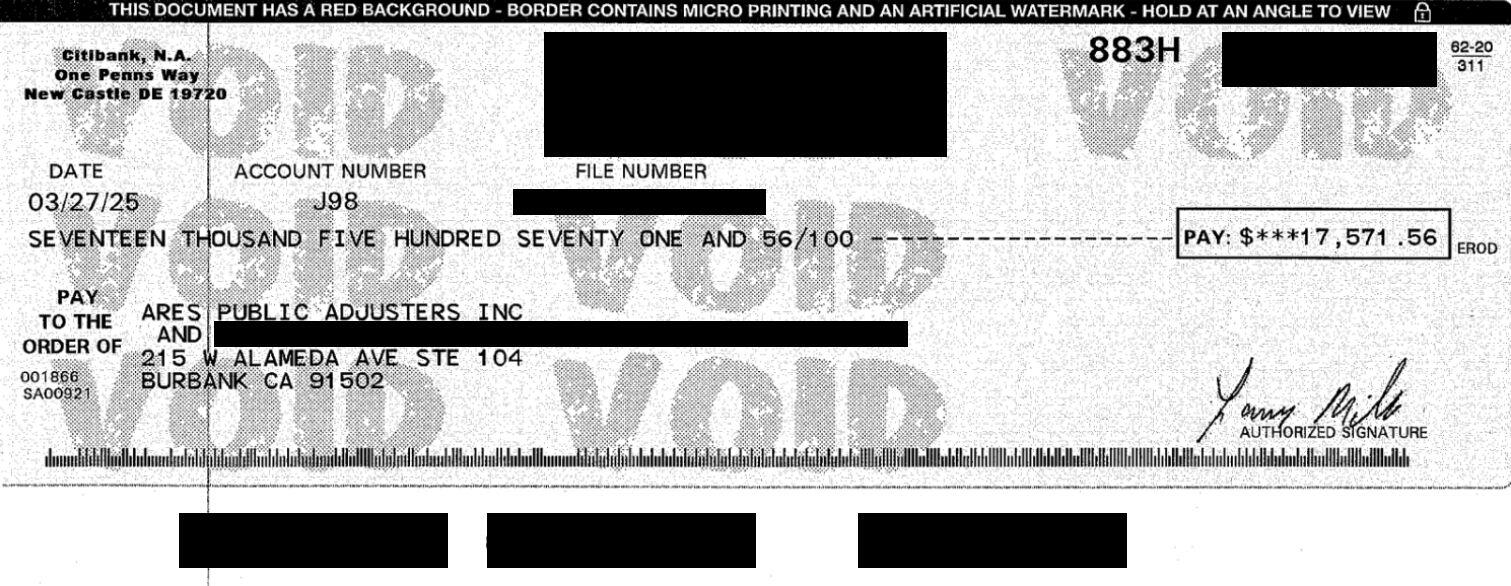

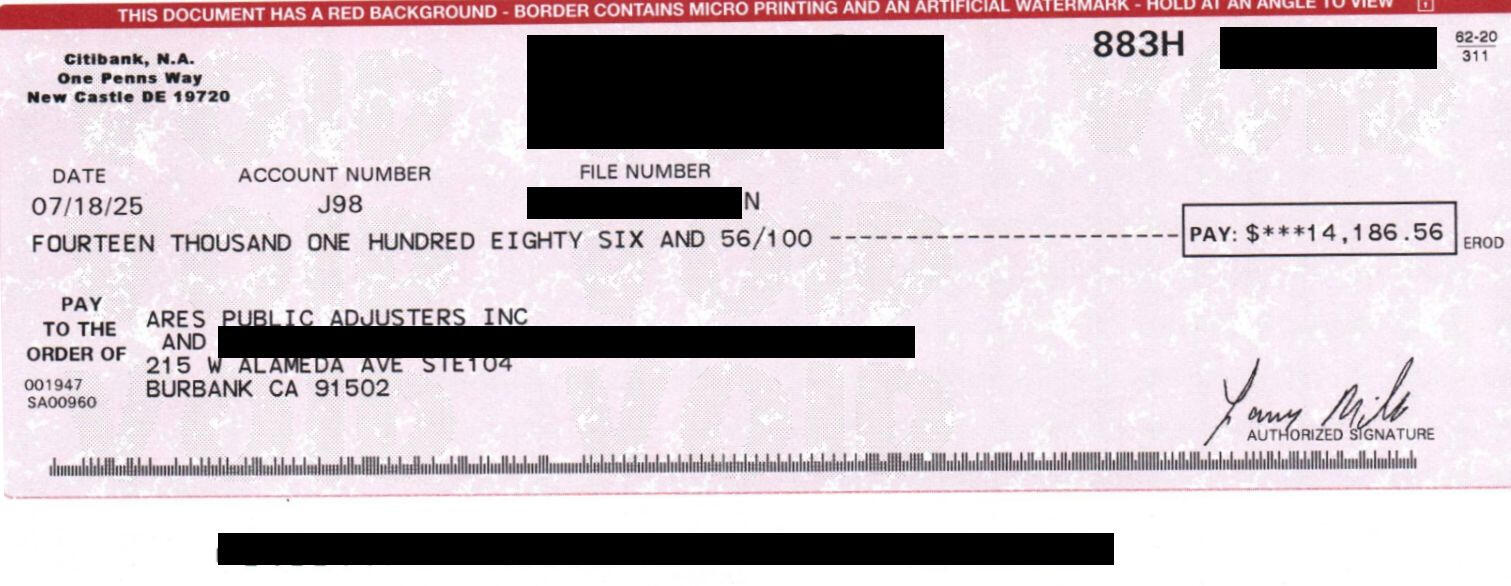

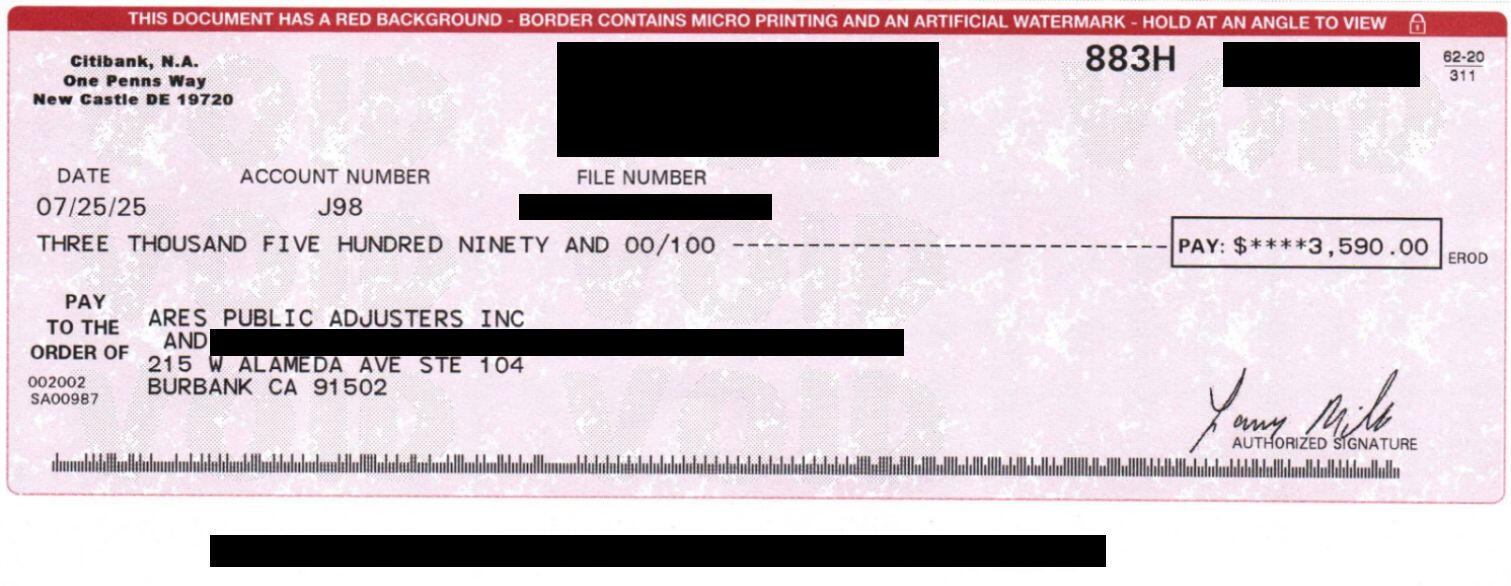

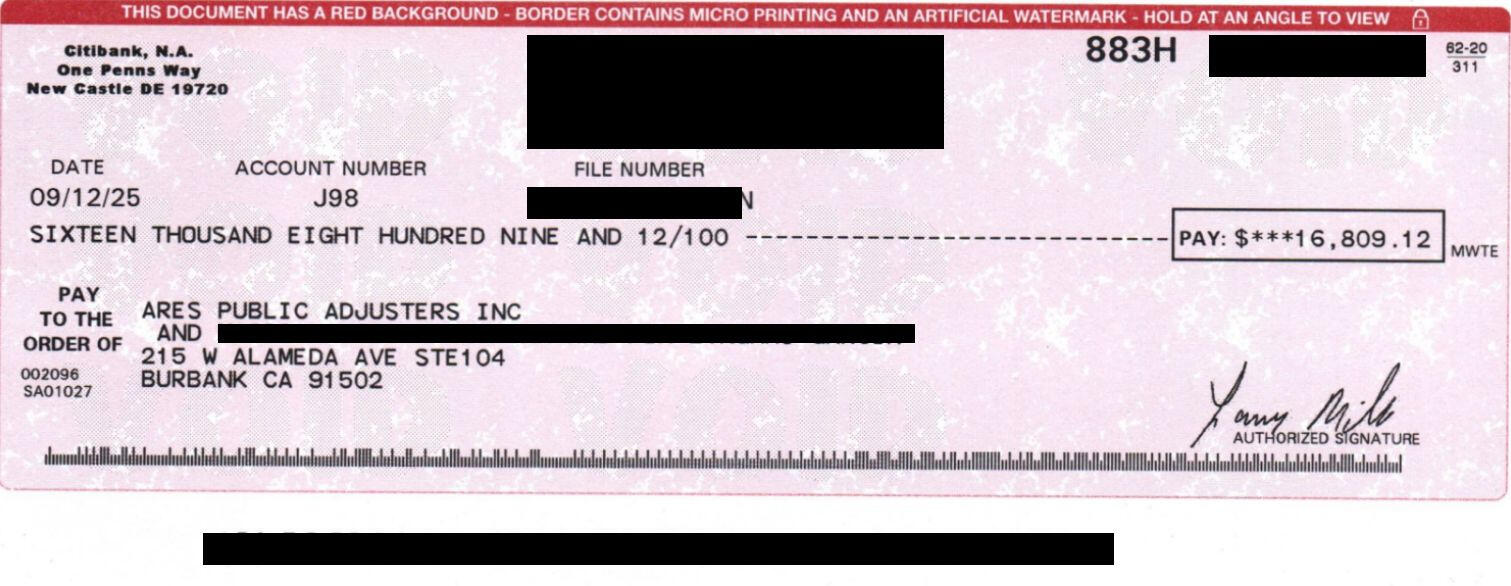

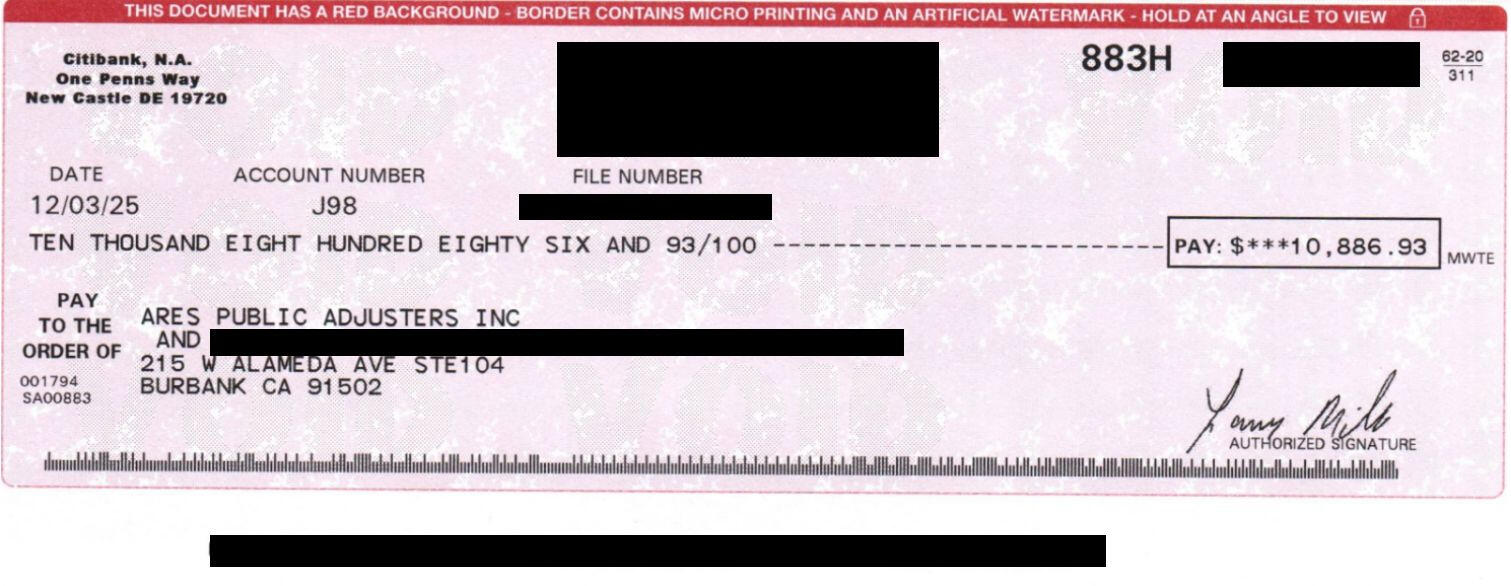

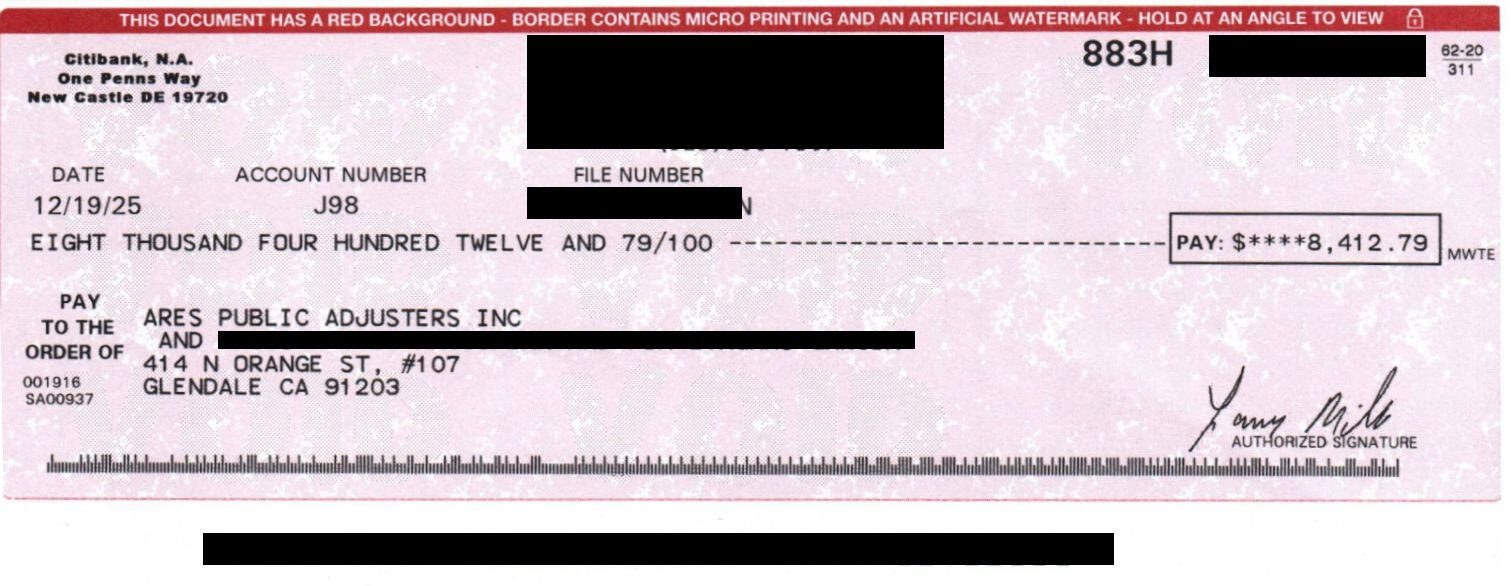

Through continued documentation, negotiation, and the appraisal process, the claim ultimately resulted in multiple supplemental payments issued to the policyholder for both the dwelling and smoke-affected contents.Confirmed payments issued to the insured included:$17,571.56 - Initial Dwelling Cleaning$14,186.56 - Dwelling Cleaning Supplement$3,590.00 - Hygienist Testing$16,809.12 - Dwelling Cleaning Supplement$10,886.93 - Contents Cleaning$8,412.79 - Dwelling Cleaning SupplementThe total settlement amount was $71,456.96

Key Takeaway

Smoke claims following wildfire events often involve significant scope disagreements related to cleaning, deodorization, exterior contamination, and contents remediation. In this case, careful documentation, persistence with the carrier, and the use of the appraisal process helped ensure that the insured received additional funds necessary to address the full extent of the smoke damage.This case highlights the importance of professional representation when navigating complex wildfire smoke claims, especially when exterior components such as roofing systems and solar panels require specialized cleaning and restoration.

Initial Dwelling Cleaning Check

Dwelling Supplement Cleaning Check

Hygienist Testing Check

Dwelling Supplement Cleaning Check

Contents Cleaning Check

Dwelling Cleaning Supplement Check

Settled $311,307.12

The Loss Occurs

In April 2024, a residential water loss occurred after a dishwasher supply line failed. Water spread through the kitchen and into surrounding areas, damaging flooring, cabinetry, finishes, and personal property. The home became unlivable, forcing the family to relocate.

Dishwasher Failed Supply Line

Kitchen Area

Early Pushback

During the carrier’s initial inspection, the adjuster claimed there was mold present near the dishwasher. This was immediately used as a basis to question coverage and delay the claim. No proper mold testing supported this position.

Challenging the Mold Claim

We reviewed the affected areas and demonstrated that the condition identified by the carrier was not mold. Documentation, photos, and expert input showed the damage was consistent with water intrusion from the failed supply line. The carrier ultimately reversed course and acknowledged the loss as covered.

Thermal Imaging from Inspection

Expanding the Scope

Once coverage was confirmed, it became clear the damage extended well beyond a small kitchen repair. Water had affected flooring throughout the home, along with baseboards, paint, and connected finishes. We pushed for a full scope that reflected how water actually behaves, not a limited patch repair. The carrier agreed to pay for full floor replacement, repainting, and associated work.

Temporary Housing Delays

Because the home was not livable, the family secured a rental. Although loss of use coverage applied, rent payments were repeatedly delayed. Over the life of the claim, multiple rent checks were late or required reissuance. Each delay created financial strain for the insured.

Adjuster Turnover

Throughout the claim, the carrier reassigned the file multiple times. Desk adjusters and supervisors changed repeatedly. Each transition slowed progress and forced the claim to be re explained. These handoffs were a major source of delay across repairs, contents, and housing payments.

Recovering the Rent

Despite the delays, we tracked every month of displacement and pushed for full payment. We escalated when necessary and ensured the insured was paid for extended loss of use covering many months of rent. Supplemental payments were issued to correct earlier underpayments.

Disputes Over Repairs and Contents

As the claim progressed, disagreements arose over cabinetry, contents, emergency services, and pack out costs. Vendor estimates understated the real scope of work. Multiple supplements were required, and some payments were initially issued under the wrong coverage. Each error had to be corrected.

Invoking Appraisal

By late 2024, the rebuild estimate remained significantly underpaid. After months of stalled negotiations, the appraisal clause was invoked. Independent appraisers reviewed the loss, inspected the property, and evaluated the true cost of repairs.

Final Resolution

In early 2025, the appraisal award and final supplements were issued. Remaining rent payments followed. With all categories resolved, the claim was fully settled.

The Outcome

Total recovery on this claim was $311,307.12.

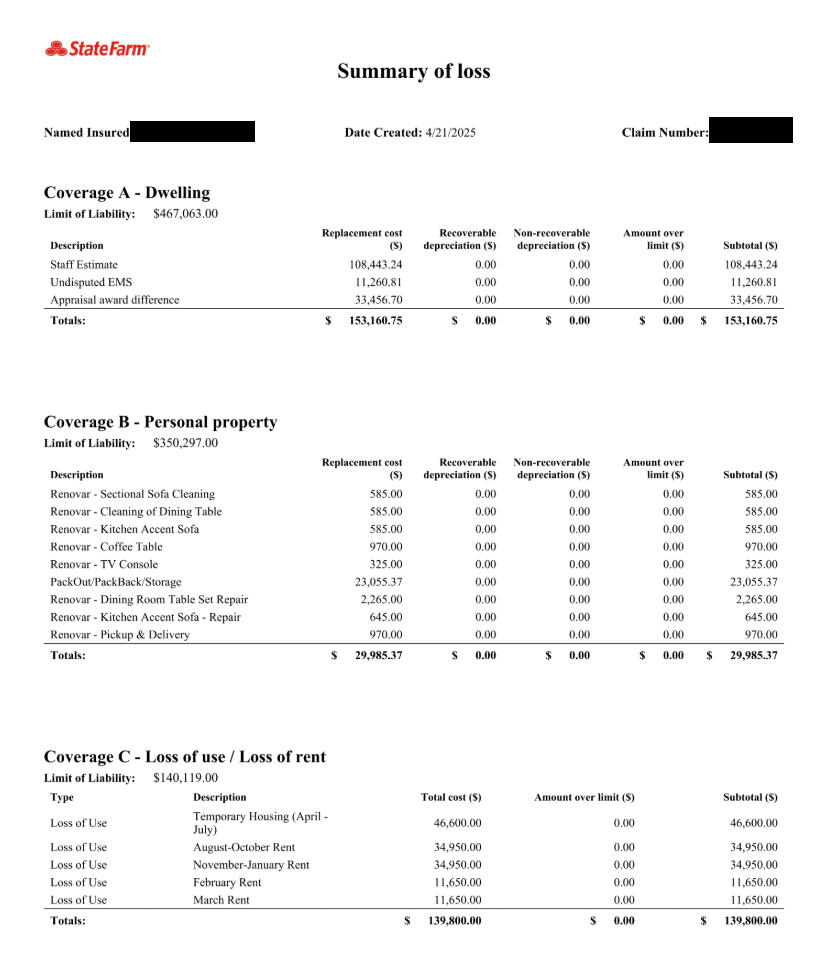

Summary of Loss

Initial Rebuild Check

Initial Contents Check

Emergency Mitigation Services Check

Packout & Packback Check

Monthly Rent Check

Privacy Policy

Effective Date: May 25, 2026Ares Public Adjusters values your privacy. This Privacy Policy explains how we collect, use, store, and protect personal information when you visit aresclaims.com, contact us, submit a form, or use our public adjusting services.Information We CollectWe may collect the following information:Contact information: name, phone number, email address, mailing address, and property address.Claim-related information: insurance policy information, claim numbers, date of loss, damage details, photos, estimates, documents, communications, and other information needed to evaluate or assist with a property insurance claim.Website information: IP address, browser type, device information, pages visited, form submissions, and similar usage data collected through cookies, analytics tools, or similar technologies.Communication information: emails, text messages, phone call details, consultation requests, and other information you choose to provide.We do not collect more information than reasonably necessary to operate our business, respond to inquiries, and provide public adjusting services.How We Use InformationWe may use personal information to:Provide public adjusting services.Review, document, prepare, manage, and negotiate property insurance claims.Communicate with clients, prospective clients, insurance companies, contractors, consultants, and other claim-related parties.Respond to questions, consultation requests, and website form submissions.Maintain business records and improve our services.Protect our legal rights, comply with legal obligations, and prevent fraud or misuse.Send service-related communications. We may also send marketing communications where permitted by law, and you may opt out at any time.How We Store InformationAres Public Adjusters uses its own custom software to store and manage client and claim information. We do not use Salesforce.We may also use trusted service providers for website hosting, data storage, email, communications, analytics, security, and other business operations. These providers are only permitted to use information as needed to provide services to us or as required by law.How We Share InformationWe do not sell personal information.We may share information when reasonably necessary with:Insurance companies, adjusters, contractors, consultants, experts, attorneys, or other parties involved in a claim.Service providers who help us operate our website, software, communications, storage, and business systems.Government agencies, regulators, courts, or law enforcement when required by law.Other parties with your consent or at your direction.If we use advertising or analytics tools that qualify as “sharing” under California privacy law, we will provide any required opt-out method.Cookies and TrackingOur website may use cookies and similar technologies to operate the site, understand visitor activity, improve performance, and support marketing or analytics.Some browsers offer “Do Not Track” signals. Our website may not respond to all browser-based Do Not Track signals. Where legally required, we will honor applicable opt-out preference signals or provide another method to exercise privacy choices.California Privacy RightsCalifornia residents may have the right to:Know what personal information we collect, use, disclose, sell, or share.Request access to personal information.Request correction of inaccurate personal information.Request deletion of personal information, subject to legal and business exceptions.Opt out of the sale or sharing of personal information, if applicable.Limit the use of sensitive personal information, if applicable.Not be discriminated against for exercising privacy rights.To make a privacy request, contact us using the information below. We may need to verify your identity before completing a request. Authorized agents may submit requests on behalf of California residents where permitted by law.Data RetentionWe retain personal information for as long as reasonably necessary to provide services, manage claims, maintain business records, comply with legal obligations, resolve disputes, and enforce agreements.SecurityWe use reasonable administrative, technical, and physical safeguards to protect personal information. No website, software system, or method of electronic storage is completely secure, so we cannot guarantee absolute security.Children’s PrivacyOur website and services are not directed to children under 13. We do not knowingly collect personal information from children under 13.Updates to This PolicyWe may update this Privacy Policy from time to time. The updated version will be posted on this website with a revised effective date.Contact UsFor questions or privacy requests, contact:Ares Public Adjusters

414 N Orange St Unit 107

Glendale, CA 91203

Phone: (818) 918-3332

Email: info@aresclaims.com

Terms & Conditions

Effective Date: May 25, 2026Welcome to the website of Ares Public Adjusters. These Terms and Conditions explain the rules for using our website, contacting our firm, and understanding the general nature of our public adjusting services.By using this website, submitting a form, contacting us, or requesting information, you agree to these Terms and Conditions. If you do not agree, please do not use this website.About Ares Public AdjustersAres Public Adjusters is a public adjusting firm serving Los Angeles and surrounding areas. We represent insured policyholders, not insurance companies.Our services may include reviewing insurance policies, documenting property damage, preparing claim support, communicating with insurance companies, and negotiating property insurance claims on behalf of policyholders.Website Information OnlyThe information on this website is provided for general informational purposes only. It is not legal advice, insurance coverage advice, tax advice, or a guarantee of any claim result.Every insurance claim is different. Claim outcomes depend on the policy, facts, damages, documentation, carrier position, applicable law, and other claim-specific issues.No Public Adjuster Relationship Until Signed ContractContacting Ares Public Adjusters, submitting a website form, calling us, emailing us, or receiving a consultation does not automatically create a public adjuster-client relationship.A public adjuster-client relationship is created only after both the policyholder and Ares Public Adjusters sign a written public adjuster contract.If there is any conflict between these website Terms and Conditions and a signed public adjuster contract, the signed contract controls.Fees and CompensationAny fee, commission, or compensation owed to Ares Public Adjusters will be stated in the signed public adjuster contract.Ares Public Adjusters does not charge a public adjusting fee unless authorized by the client and allowed under the signed contract and applicable law.No Guarantee of Insurance PaymentAres Public Adjusters works to properly document, prepare, present, and negotiate claims. However, we do not guarantee that an insurance company will pay a claim, increase a claim payment, approve coverage, or resolve a claim within a specific time.Insurance companies make coverage and payment decisions based on the policy, claim investigation, documentation, and their interpretation of the loss.Client ResponsibilitiesClients and prospective clients are responsible for providing accurate, complete, and truthful information.This includes insurance policies, claim numbers, communications from the insurance company, photos, receipts, estimates, inventories, repair records, mortgage information, and any other documents relevant to the claim.Ares Public Adjusters may rely on the information provided by the client when preparing or presenting a claim.Use of Custom SoftwareAres Public Adjusters may use its own custom software to manage claim information, documents, communications, and internal workflows.Clients may be asked to provide documents, photos, signatures, or claim information electronically. By communicating with us electronically, you consent to electronic communication unless you tell us otherwise in writing.Third PartiesDuring a claim, Ares Public Adjusters may communicate with insurance companies, insurance adjusters, contractors, consultants, engineers, mitigation companies, appraisers, attorneys, mortgage companies, and other claim-related parties when reasonably necessary.Ares Public Adjusters is not responsible for the work, pricing, delays, statements, warranties, or conduct of third-party vendors unless specifically agreed in writing.Not a Contractor or Repair CompanyAres Public Adjusters is a public adjusting firm. We do not act as a general contractor, construction company, restoration company, remediation company, engineer, architect, or repair warranty provider.Any repair, mitigation, construction, or professional service agreement with a third party is separate from Ares Public Adjusters.Website UseYou agree not to misuse this website. You may not attempt to hack, damage, overload, scrape, copy, reverse engineer, interfere with, or gain unauthorized access to the website, software, forms, systems, or data of Ares Public Adjusters.You may not use this website to submit false information, spam, unlawful content, or information belonging to another person without authorization.Intellectual PropertyThe text, design, branding, logo, graphics, photos, videos, content, and other materials on this website are owned by or licensed to Ares Public Adjusters unless otherwise stated.You may view and print website pages for personal, non-commercial use. You may not copy, reproduce, sell, modify, distribute, or use website content for commercial purposes without written permission from Ares Public Adjusters.Third-Party LinksThis website may contain links to third-party websites or services. These links are provided for convenience only.Ares Public Adjusters does not control and is not responsible for third-party websites, content, policies, security, services, or business practices.PrivacyUse of this website is also governed by our Privacy Policy. Please review the Privacy Policy to understand how we collect, use, store, and protect personal information.Limitation of LiabilityTo the maximum extent permitted by law, Ares Public Adjusters is not liable for damages arising from use of this website, inability to use this website, reliance on website information, technical issues, third-party links, or unauthorized access caused by factors outside our reasonable control.This limitation does not limit any rights a client may have under a signed public adjuster contract or applicable law.IndemnificationYou agree to hold Ares Public Adjusters harmless from claims, losses, damages, liabilities, and expenses arising from your misuse of the website, submission of false information, violation of these Terms and Conditions, or violation of another person’s rights.Changes to These TermsAres Public Adjusters may update these Terms and Conditions from time to time. Updates will be posted on this website with a revised effective date.Continued use of the website after changes are posted means you accept the updated Terms and Conditions.Governing LawThese Terms and Conditions are governed by the laws of the State of California, without regard to conflict of law rules.To the extent legally permitted, any dispute related to this website or these Terms and Conditions will be handled in California. These Terms do not override any dispute-resolution terms in a signed public adjuster contract.Contact UsFor questions about these Terms and Conditions, contact:Ares Public Adjusters

414 N Orange St Unit 107

Glendale, CA 91203

Phone: (818) 918-3332

Email: info@aresclaims.com

Water Damage Public Adjusting Firm

We Work For You. Not the Insurance Company.

Get What You Deserve and Minimize Your Stress: Your Trusted Public Adjusting Firm

Water Damage Case Studies

Failed Dishwasher Supply Line

(Water Damage)

Settled $311,307.12Ceiling Pipe Burst

(Water Damage)

Settled $115,406.37

Don't Settle For Less With The Insurance Companies

Vandalism & Burglary

Get your Free Consultation

Compensation You Deserve

We ensure our clients receive the compensation they deserve. Here are some examples of claims we've expertly managed, showcasing our commitment to securing the best possible outcomes for our clients.

What We Do

Water Damage Assessment and Documentation

Our experienced team will assess the extent of the water damage to your property and thoroughly document the damages, ensuring nothing is overlooked.

Water Damage Insurance Claims Management

We will work closely with your insurance company, ensuring you receive the maximum compensation you deserve. Our experts will handle all negotiations on your behalf.

Quick Resolution

Our goal is to expedite the claims process, so you can focus on restoring your home and getting your life back to normal as soon as possible.

Why Choose Us?

Specialized Expertise in Water Damage

Our team of public adjusters specializes in water damage claims and has a deep understanding of the insurance industry.

Personalized Water Damage Claim Services

We treat every client with the care and attention they deserve, providing tailored solutions for your specific situation.

Maximizing Your Water Damage Compensation

Our goal is to maximize your claim, ensuring you're properly compensated for your losses.

Frequently Asked Questions

What should I do immediately after discovering water damage in my home?

After discovering water damage, it's crucial to take prompt action. First, ensure your safety by turning off electricity and gas if it's safe to do so. Then, try to stop the source of water, if possible.

Do I need a public adjuster for my water damage claim, or can I handle it myself?

While you can file a claim on your own, having a public adjuster on your side can significantly benefit you. We have the expertise to navigate the complex insurance claims process, ensuring you receive fair compensation for your losses.

What should I document when filing a water damage claim?

When filing a claim, document as much as you can. Take photos and videos of the damage, do not contact your insurance company as we will call them on your behalf. Save receipts for any expenses related to the cleanup and restoration of your property.

How long does it take to settle a water damage claim?

The duration of claim settlement can vary depending on the complexity of your case and your insurance company's policies. We work to expedite the process, but it's essential to be patient as insurance claims can take some time to resolve.

Will my insurance premium increase if I file a water damage claim?

Filing a legitimate water damage claim typically won't result in a premium increase, as it is considered a non-fault claim.

What if my insurance claim is denied or underpaid?

If your claim is denied or underpaid, our experienced public adjusters can help you dispute the decision, providing evidence and negotiating with your insurance company to ensure you receive fair compensation.

Can I prevent water damage in the future?

Yes, there are steps you can take to prevent water damage, such as regular maintenance of your plumbing and roof, installing a sump pump, and ensuring proper drainage around your property. We can provide you with tips and resources to protect your home from future water damage.

Maximum Settlement

Our team's expertise and dedication have consistently resulted in delivering the maximum possible settlement amount, ensuring our clients receive the compensation they truly deserve.

Fire/Smoke Damage Public Adjusting Firm

We Work For You. Not the Insurance Company.

Get What You Deserve and Minimize Your Stress: Your Trusted Public Adjusting Firm

Smoke Damage Case Studies

Altadena Fire 2026

(Smoke Damage)

Settled: $71,456.96

Palisades Fire 2026

(Smoke Damage)

Settled $186,960.04

Altadena Fire 2026

(Smoke Damage)

Settled: $93,244.73

Don't Settle For Less With The Insurance Companies

Vandalism & Burglary

Get your Free Consultation

Compensation You Deserve

We ensure our clients receive the compensation they deserve. Here are some examples of claims we've expertly managed, showcasing our commitment to securing the best possible outcomes for our clients.

Our Process

Damage Assessment and Documentation

Our experienced team will assess the extent of the smoke and fire damage to your property and meticulously document the damages to support your insurance claim.

Insurance Claims Management

We will work closely with your insurance company to ensure you receive the maximum compensation you deserve. Our experts will handle all negotiations on your behalf.

Quick Resolution

Our goal is to expedite the claims process, so you can begin the process of restoring your home as soon as possible.

Why Choose Us?

Specialized Expertise in Fire and Smoke Damage

Our team of public adjusters specializes in smoke and fire damage claims and has a deep understanding of the insurance industry.

Personalized Fire and Smoke Damage Claim Services

We treat every client with the care and attention they deserve, providing tailored solutions for your unique situation.

Maximizing Your Fire and Smoke Damage Compensation

Our goal is to maximize your claim, ensuring you're properly compensated for your losses.

Frequently Asked Questions

Is smoke and fire damage typically covered by homeowner's insurance policy?

In most cases, smoke and fire damage is covered by homeowner's insurance policies. However, it's essential to review your policy to understand the extent of your coverage and any limitations.

What should I do immediately after a fire in my home is extinguished?

After a fire, it's vital to ensure your safety and the safety of your family. Contact the fire department if you haven't already, and then document the damage with photographs. It's also crucial for our team to conduct an inspection in order to properly document all damages

How can a public adjuster assist with my smoke and fire damage claim?

Our public adjusters will assess the damage, compile detailed evidence, and negotiate with your insurance company to ensure you receive fair compensation for your losses. We're your advocates throughout the claims process.

What if my insurance claim is denied or underpaid?

If your claim is denied or underpaid, we can help you dispute the decision, providing strong evidence and negotiating with your insurance company to ensure you receive a fair settlement.

How long does it take to settle a smoke and fire damage claim?

The duration of claim settlement can vary depending on the complexity of your case and your insurance company's policies. We work to expedite the process, but it's essential to be patient, as these claims can take time to resolve.

Can I prevent smoke and fire damage in the future?

While accidents can happen, we can provide you with tips and resources to minimize the risk of smoke and fire damage in your home, such as proper fire safety measures and maintenance.

Maximum Settlement

Our team's expertise and dedication have consistently resulted in delivering the maximum possible settlement amount, ensuring our clients receive the compensation they truly deserve.

Wind Damage Public Adjusting Firm

We Work For You. Not the Insurance Company.

Get What You Deserve and Minimize Your Stress: Your Trusted Public Adjusting Firm

Don't Settle For Less With The Insurance Companies

Water Damage

Fire, Smoke & Ash Damage

Vandalism & Burglary

Get your Free Consultation

Compensation You Deserve

We ensure our clients receive the compensation they deserve. Here are some examples of claims we've expertly managed, showcasing our commitment to securing the best possible outcomes for our clients.

What We Do

Comprehensive Roof Damage Assessment

Our expert team conducts a detailed assessment of wind damage to roofs, ensuring thorough documentation for your insurance claim. This critical step is key in securing the maximum compensation for wind-related roof damages.

Efficient Insurance Claims Management for Wind Damage

Navigating insurance claims for wind damage can be complex. Our public adjusters work diligently with your insurance company, advocating for your right to full compensation. We handle all aspects of the negotiation process for your wind damage claim.

Swift Claims Resolution for Wind-Damaged Roofs

Speed is essential in resolving wind damage claims. Our goal is to fast-track your insurance claim, facilitating quick repairs or replacements for your wind-damaged roof.

Why Choose Us?

Specialized Expertise in Wind Damage

Our team, specializing in wind damage insurance claims, possesses deep knowledge of the insurance industry, particularly in wind damage scenarios.

Personalized Wind Damage Claim Services

We offer customized solutions for each wind damage case, providing the dedicated attention you need.

Maximizing Your Wind Damage Compensation

Our aim is to secure the maximum possible compensation for your wind-damaged roof.

Frequently Asked Questions

Is wind damage to my roof covered by my homeowner's insurance policy?

In most cases, wind damage is covered by homeowner's insurance. However, the extent of coverage and deductibles can vary. We can help you review your policy and understand your coverage.

What should I do immediately after discovering roof damage from wind?

After discovering roof damage, it's crucial to prevent further damage by covering exposed areas if safe to do so. We have well experienced roofing contractors that we can refer you to.

How can a public adjuster assist with my wind damage claim?

Our public adjusters will assess your roof's damage, gather evidence, and negotiate with your insurance company to ensure you receive the maximum compensation possible. We're your advocates in the claims process.

Will filing a wind damage claim increase my insurance premiums?

Filing a legitimate wind damage claim is typically considered a non-fault claim and shouldn't result in a premium increase.

What if my insurance claim is denied or underpaid?

If your claim is denied or underpaid, we can help you dispute the decision, providing evidence and negotiating with your insurance company to ensure you receive fair compensation.

How can I prevent wind damage to my roof in the future?

We can provide you with tips and resources on how to safeguard your roof against wind damage, such as regular maintenance, reinforced shingles, and proper anchoring methods.

Maximum Settlement

Our team's expertise and dedication have consistently resulted in delivering the maximum possible settlement amount, ensuring our clients receive the compensation they truly deserve.